|

|

All that Glitters: Gold and Silver

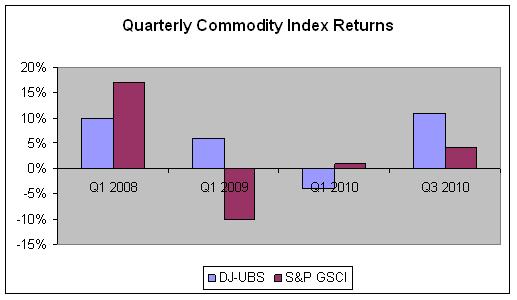

Commodity indexes did better in the third quarter than the first half of the

year, as Barclays Capital analyst Kevin Norrish pointed out in a report.

Overall, two key benchmarks, the S&P Goldman Sachs Commodity Index and the Dow

Jones UBS index, have been less volatile in 2010 than in the previous two years,

a period that included steep drawdowns during the 2008-2009 crisis and the

subsequent partial recovery.

Commodities started this year with losses but turned positive in July (table

below). One of the intriguing patterns of the past five months is the leading

role of precious metals in the commodity rally. Agriculture was also a

substantial profit generator, but gold and silver led the commodity pack in

returns through September. And in October, gold and silver rose to new highs.

In long-only investments, an uncertain macroeconomic climate kept interest

focused on agriculture and precious metals, according to the Barclays Capital

report. In August, withdrawals outpaced investments in commodities at large.

"Most of the decline was due to a reduction in institutional and retail investor

exposure reflected in a $5 billion reduction in broad commodity exposure via

index swaps," says Barclays.

In dramatic contrast, demand for gold investments recovered quickly and money

flowed to gold exchange-traded funds. Gold investing has been a major part of

commodity investments this year. Barclays found that gold accounted for about

one-third of the total $29 billion new commodity investments year-to-date as of

September.

"The enthusiasm for physical exposure to gold shows investors are still very

uneasy about the future," Mr. Norrish comments.

Futures Markets

Hedge funds and commodity trading advisors tracked the rally, keeping large net

long positions in precious metals since March. They bought silver and palladium

as well as gold. Net long positions in palladium and silver futures were near

all-time highs. Net positions in gold futures were the largest since early 2010.

Trend followers are riding on the up trends.

While both silver and gold continue to surge, there is an interesting change

in the relationship between the two metals. The price ratio of gold to silver

has been falling and is now at its lowest since before the collapse of Lehman

Brothers in 2008, according to GoldCore-one ounce of gold buys around 56.5

ounces of silver. But that is still high compared to 1980, when the Hunt

Brothers cornered the silver market

Silver has several advantages. While the metal is a possible substitute for gold

as a hedge against currency depreciation, it is still used as an industrial

input. Global growth creates industrial demand for silver. What is more, silver

is cheap by historic standards. Thus there is room for the relative price of

gold to silver to go down further.

Passive vs. Active Gold

The gold rally has led to forecasts of a bubble in the metal. However, the rush

to gold is arguably an attempt by investors to protect themselves against the

weakening United States dollar.

Strangely, the Federal Reserve could be seen as a the patron saint of gold bugs!

The Fed's zero interest rate policy and quantitative easing to stimulate growth

has made US assets - and by implication the US dollar - less attractive. A

second round of QE appears to be in the works-see Futures Lab in this issue.

As a result billions of dollars have moved into gold exchange-traded funds and

other long-only investments. Paulson & Co and Harbinger, prominent hedge funds

but not big commodity players, are among big buyers of gold ETFs.

A small portion of the money flowing to gold has gone to actively managed gold

funds and commodity trading advisors. CTAs argue that they have an advantage

over long-only commodity investments-they can go short to take advantage of

declining markets. If there is a significant downward correction in gold,

whether because a bubble collapses or people see better opportunities elsewhere,

CTAs and other active managers can still make profits, whereas index investments

and ETFs are sure to lose.

That said, gold is a tough market to make money in, whether you use a passive

index or managed futures, go long or short. While many now regard it as a safe

haven against inflation and currency depreciation, historically gold investing

was anything but safe. Before the steep rise of the past decade, it was a

persistent loser for some 20 years.

Notwithstanding the argument that active management can exploit market declines,

there is no shortage of CTAs who've been burnt by gold. One gold expert lost

more than 44% last November. The December gain made up for the November

drawdown, but the experience shows how perilous this market can be.

The metal does not necessarily move in line with other commodities. That can

work in gold investors' favor- in the crisis year of 2008 precious metals eked

out a small positive return even as the energy-dominated Goldman Sachs Commodity

Index lost 47%. But at other times the non-correlation works against gold. For

instance, during the stock market bust of 2000 precious metals went down while

the GSCI returned close to 50%.

Gold certainly can have a place in a diversified long/short CTA portfolio but in

the immediate future other commodities have more potential. Grains, rather than

gold, look promising in the short term. Barclays expects high prices in a number

of commodities in the fourth quarter - oil, base metals and some agricultural

products - but not in gold.

Net positions in grain futures spiked in the summer as headlines announced

Russia's export ban on wheat and remain at near-record highs as bad harvests

point to continuing strength. See the August 17, 2010, issue of Opalesque

Futures Intelligence for an interview with agriculture specialist Brooks Brown

of Cypress Capital.

Source: Barclays Capital

|

RSS

RSS

{kind=link}